Does a refi make cents?

I got a call recently from an investor named Brad that had a conundrum. He was looking at refinancing a mortgage from a 30-year fixed ARM (adjustable rate mortgage) to a 15-year fixed mortgage.

A fixed adjustable rate mortgage sounds like an oxymoron.

They work like this- for the first five to ten years the rate is fixed. After that, it can adjust each year.

These little guys are tricky because buyers have no way of knowing what rates will be like in the future. Brad started out at 5.75 percent eleven years ago. Today, his rate is down in the threes, but, he recently received a letter saying it will go up to four percent next year and could climb every year to as high as 10.75 percent.

Obviously Brad started looking for a new mortgage. He called around and found he could lock in a 20 year fixed rate at only 3.875 percent. BAM!

That sounds like a no-brainer. So why was he calling me?

Estimated closing costs on this mortgage were going to run $8,500. Because of that, he couldn’t tell if this was a good deal.

As we were talking, I asked him to run the numbers in his financial calculator. He said he didn’t know how.

If you don’t know how to run a financial calculator, don’t feel bad- many investors don’t- but you really should learn how. If you know how to use one, a financial calculator will make you a ton of money.

I’d like to walk you through Brad’s numbers and show you why he needed to evaluate this deal.

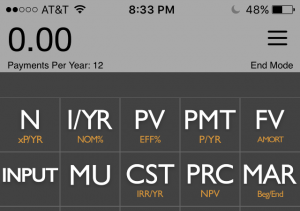

There are five inputs on the top of a financial calculator. They are as follows:

N= number of payments in months, I/YR= interest or yearly return, PV= present value of the loan or investment, PMT= payments and FV= future value.

So for Brad’s first loan, the initial fixed period looked like this:

N=360 (30 yrs), I/YR= 5.75, PV= 139,656.94, PMT=-815 and FV=0.00

Note: When dealing with loans, PV and PMT can and should be positive or negative. If you’re receiving money, they’ll be positive. If you’re paying money out, they’ll be negative.

In this scenario, Brad received $139,656.94 to buy a house. So the PV value is positive. However, he had to pay $815 per month back to the bank. Since the money was leaving him, the PMT value is negative.(This is very important. If you get the positive and negative values confused, the calculator will give you an error message.)

With his new rate, Brad’s new payment will be $690. That looks like this:

N=240 (20 yrs), I/YR= 3.875, PV= 115,112.43, PMT=-690 and FV=0.00

Note: PV changed due to pay down on the mortgage over the 11 years.

Remember how I said Brad was focused on the $8,500 in closing costs? Using the financial calculator he quickly found out what the return on his money will be. He just had to know four out of the five pieces of information.

In this case, he needed to know how much refinancing would save, or pay, him each month: it’ll save him $125 per month. (I arrived here by subtracting the new payment of $690 for the original payment of $815)

Now we can see if spending the $8,500 is a wise decision.

Brad will get paid $125 a month for 20 years and it’ll cost $8,500 to do it.

Let’s put that into the calculator and solve for I/YR:

N=240 (20 yrs), I/YR= ?, PV= -8,500, PMT=125 and FV=0.00

By refinancing, Brad will earn a return of 17.05 percent. That ain’t bad!

But it gets better. It turns out his out-of-pocket cost at closing will be only $3,800. Substitute that for PV and it makes his return 39.46 percent!

This refi didn’t just make cents, it made lots of dollars as well. And that’s why it pays to learn how to run a financial calculator.

Joe and Ashley English invest in real estate in Northwest Georgia. For more information or to ask a question, go to www.cashflowwithjoe.com